May 29, 2025

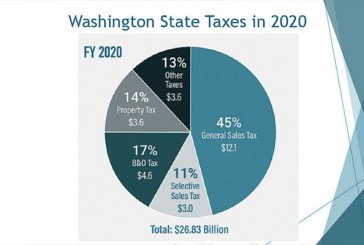

Is the current Washington state tax structure unfair? Washingtonians are not very trusting of government ...

Is the current Washington state tax structure unfair? Washingtonians are not very trusting of government promises. ...